Revenue-Based Financing for Game and App Developers

Revenue-Based Financing for Game and App Developers

BEST PRACTICES

Sep 2, 2022

Sep 2, 2022

Sep 2, 2022

4 min read

4 min read

4 min read

When you decide to take your app or game company to the next level (no pun intended), it often means that it's time to look into how to finance it. But with so many options to choose from, ranging from traditional business loans to equity financing to publishing and beyond, entering this stage in your business's growth can quickly turn from an exciting milestone to a nerve-wracking decision.

Chances are that when you think "financing," you imagine one of three things: either you trade a stake in your company for an investment (equity financing), get a bank loan (debt financing), or secure a publishing deal that comes with an advance.

But there's another option that you may not have heard of: revenue-based financing. This financing structure allows for greater flexibility and affordability without having to give up any stake in your company or creative ownership of building games and apps.

What is revenue-based financing?

Revenue-based financing (RBF) is a financing structure in which a company agrees to pay a percentage of its monthly revenue to a capital provider in exchange for a financing. Once the company has paid back the full amount, the company has no remaining obligations to the capital provider. However, if they like working with each other, they can continue developing their relationship through further financing agreements for continued scaling.

Let's look at an example with very simple numbers to make this a bit clearer. Let's say you run a gaming company that makes $50,000/month in revenue, and a capital provider offers to give you an advance for $100,000 in capital at a $120,000 total repayment amount in exchange for 30% of your monthly revenue. How would this play out?

In this case, you'd pay the capital provider $15,000 every month (0.30 * $50,000), and it would take you 8 months to pay them back entirely. But once those 8 months are up, your obligations are met, and you retain full control of your company (assuming you haven't made any other arrangements). If your revenues decrease, so does your repayment amount and vice versa.

Revenue-based financing vs debt financing

Based on the above example alone, the differences between revenue-based and debt financing like a traditional term loan may not seem immediately obvious. After all, isn't a bank loan essentially just a fixed-percentage payment made every month until the loan is paid back?

In our oversimplified example, it's true that they're pretty much identical. But in reality, no business makes exactly the same amount of revenue every month. Especially in the early stages of a business, there may be months where revenues are unusually high followed by severe and sudden downturns.

When repaying a bank loan, you have to make the same payment every month irrespective of whether your business makes $50,000 or $0 in that period. But with revenue-based funding, your monthly payment amount scales with your revenue, which can help your business stay afloat in turbulent waters.

In other words, when you take out a bank loan, it's possible that your monthly payment could end up being more than your entire revenue for the month. With RBF, that would never happen.

However, keep in mind that when you take out a traditional loan, you typically have a fixed term — i.e., you'll pay $2,000 every month for two years. But with RBF, the monthly payment fluctuations mean that it's difficult to determine when the loan amount will be paid back in full (some investors will set predetermined termination dates instead of predetermined amounts, but this is less common). Theoretically, if your revenue were high enough, you could pay back the whole thing in one month, but if business became very slow, you could end up paying back the loan in small increments over a long time period until business picks back up. In the extreme case of a month when you don’t generate any revenue, there is no repayment to the RFB partner.

This uncertainty is why it’s important to work with an RBF partner that has specific game industry experience. They’ll be able to more accurately predict how long it will take you to pay back your financing amount, which will help protect you against biting off more than you can chew.

Revenue-based financing vs equity financing

So, traditional debt financing like a term loan usually means fixed payments over a fixed timeframe while revenue-based financing means paying a fixed percentage of future revenue over an indeterminate time frame.

But what about equity financing? Equity financing solves some of the issues with debt financing, but it brings problems of its own: you're giving away a part of your company.

When you choose to go with equity financing, an investor will give you an initial investment of growth capital for your game or app. You don't have to make monthly payments at all, but you have to be prepared to give a person or a company (a venture capital firm or angel investor, for example) a percentage of direct ownership in your company. The investor will then maintain that equity either forever or until they decide to sell it — which at times may end up being to another firm that you don't want to work with.

Some venture capitalists and angel investors may want to be more involved in the workings of your game than a bank would. That means that when you enter into an equity financing agreement, you need to make sure that the investor has a similar vision of your company's future.

Revenue-based financing vs a publishing deal

Securing a publishing deal with revenue sharing is in some ways similar to equity financing in many ways. You can typically leverage publisher resources, relationships and support with UA, monetization, design, etc. While they typically provide a lot of support, they may take a large slice of the revenue pie and have input into building, managing and then scaling the game.

We’ll cover publishing deals more in depth in later articles.

Why choose revenue-based financing?

Generally, revenue-based financing is considered something of a middle ground between debt and equity financing. It's similar to debt financing in that you pay back a total financing amount you received over time without having to hand over ownership in your company, and it's similar to equity financing in that the investor makes revenue when you make revenue.

Business owners typically choose to pursue revenue-based financing when they want the flexibility of equity financing without having to give up any ownership in their company. Investors that offer revenue-based financing also tend to be more hands-off than venture capitalists but more involved than banks, offering a happy medium between the two.

Overall, revenue-based funding is particularly popular among SaaS and e-commerce companies because their revenue stream works well for this type of financing. However, it is equally well-suited to all business models with recurring revenue, like some apps and games.

Revenue-based financing example

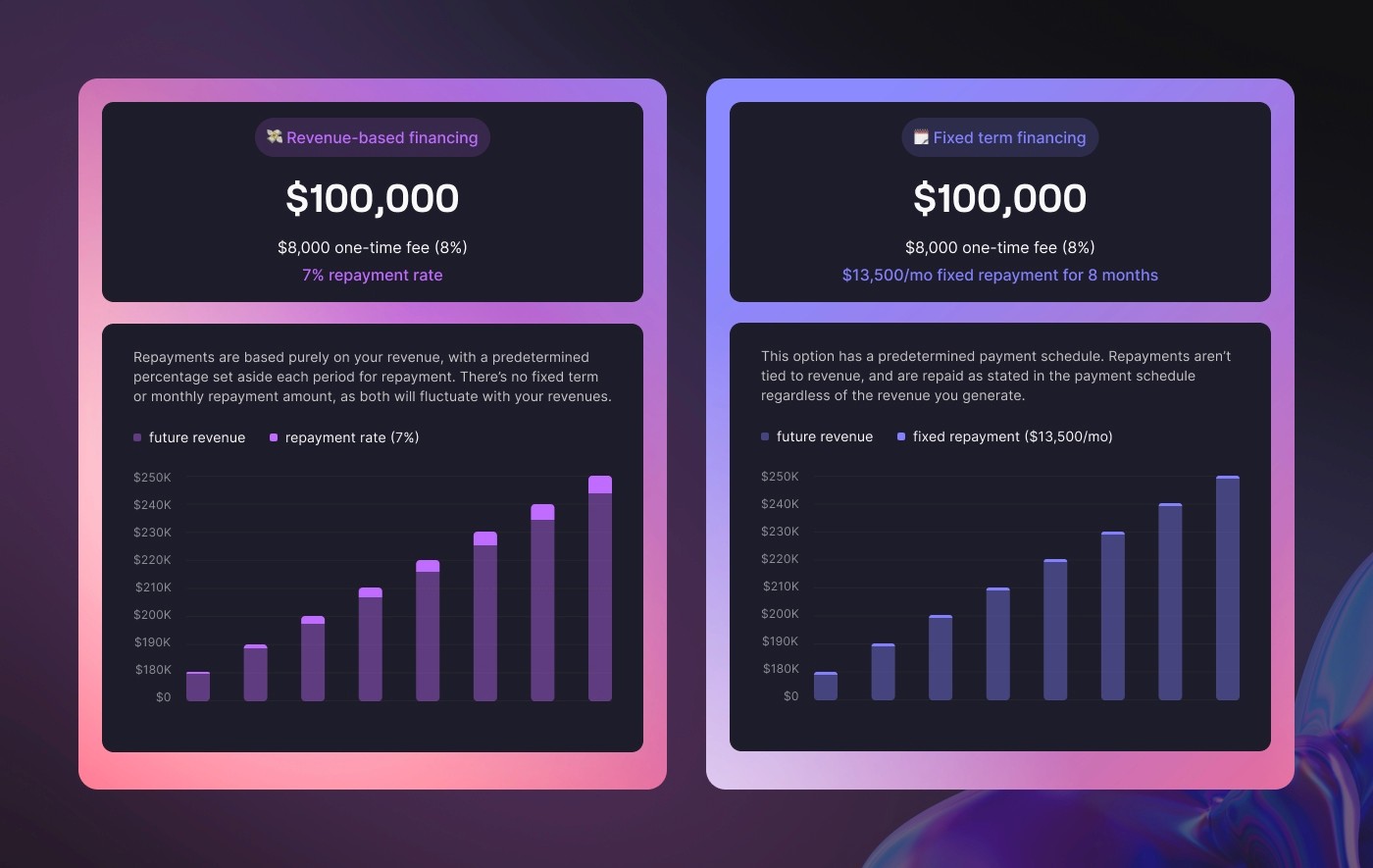

Now that we've got a better understanding of revenue-based financing, let's revisit the example from earlier with some (slightly) more realistic numbers. We'll imagine that same advance for $100,000 ($120,000 total with fees) that's paid back as 30% of future revenue.

As you can see, the amount paid each month scaled with revenue growth (or contraction), which some businesses may find preferable to having to pay back a flat fee every month.

Overall, it’s a solid alternative to banks that doesn’t force you to give up part of your company.

Choosing the right revenue-based financing firm

If you decide that RBF is the right direction to go in for your game or app financing, then it’s important to work with a company that not only knows financing in and out, but also understands the specific needs of game and app development so the terms and paybacks of the financing is in sync with the monetization mechanics and dynamics of your product.

When you decide to take your app or game company to the next level (no pun intended), it often means that it's time to look into how to finance it. But with so many options to choose from, ranging from traditional business loans to equity financing to publishing and beyond, entering this stage in your business's growth can quickly turn from an exciting milestone to a nerve-wracking decision.

Chances are that when you think "financing," you imagine one of three things: either you trade a stake in your company for an investment (equity financing), get a bank loan (debt financing), or secure a publishing deal that comes with an advance.

But there's another option that you may not have heard of: revenue-based financing. This financing structure allows for greater flexibility and affordability without having to give up any stake in your company or creative ownership of building games and apps.

What is revenue-based financing?

Revenue-based financing (RBF) is a financing structure in which a company agrees to pay a percentage of its monthly revenue to a capital provider in exchange for a financing. Once the company has paid back the full amount, the company has no remaining obligations to the capital provider. However, if they like working with each other, they can continue developing their relationship through further financing agreements for continued scaling.

Let's look at an example with very simple numbers to make this a bit clearer. Let's say you run a gaming company that makes $50,000/month in revenue, and a capital provider offers to give you an advance for $100,000 in capital at a $120,000 total repayment amount in exchange for 30% of your monthly revenue. How would this play out?

In this case, you'd pay the capital provider $15,000 every month (0.30 * $50,000), and it would take you 8 months to pay them back entirely. But once those 8 months are up, your obligations are met, and you retain full control of your company (assuming you haven't made any other arrangements). If your revenues decrease, so does your repayment amount and vice versa.

Revenue-based financing vs debt financing

Based on the above example alone, the differences between revenue-based and debt financing like a traditional term loan may not seem immediately obvious. After all, isn't a bank loan essentially just a fixed-percentage payment made every month until the loan is paid back?

In our oversimplified example, it's true that they're pretty much identical. But in reality, no business makes exactly the same amount of revenue every month. Especially in the early stages of a business, there may be months where revenues are unusually high followed by severe and sudden downturns.

When repaying a bank loan, you have to make the same payment every month irrespective of whether your business makes $50,000 or $0 in that period. But with revenue-based funding, your monthly payment amount scales with your revenue, which can help your business stay afloat in turbulent waters.

In other words, when you take out a bank loan, it's possible that your monthly payment could end up being more than your entire revenue for the month. With RBF, that would never happen.

However, keep in mind that when you take out a traditional loan, you typically have a fixed term — i.e., you'll pay $2,000 every month for two years. But with RBF, the monthly payment fluctuations mean that it's difficult to determine when the loan amount will be paid back in full (some investors will set predetermined termination dates instead of predetermined amounts, but this is less common). Theoretically, if your revenue were high enough, you could pay back the whole thing in one month, but if business became very slow, you could end up paying back the loan in small increments over a long time period until business picks back up. In the extreme case of a month when you don’t generate any revenue, there is no repayment to the RFB partner.

This uncertainty is why it’s important to work with an RBF partner that has specific game industry experience. They’ll be able to more accurately predict how long it will take you to pay back your financing amount, which will help protect you against biting off more than you can chew.

Revenue-based financing vs equity financing

So, traditional debt financing like a term loan usually means fixed payments over a fixed timeframe while revenue-based financing means paying a fixed percentage of future revenue over an indeterminate time frame.

But what about equity financing? Equity financing solves some of the issues with debt financing, but it brings problems of its own: you're giving away a part of your company.

When you choose to go with equity financing, an investor will give you an initial investment of growth capital for your game or app. You don't have to make monthly payments at all, but you have to be prepared to give a person or a company (a venture capital firm or angel investor, for example) a percentage of direct ownership in your company. The investor will then maintain that equity either forever or until they decide to sell it — which at times may end up being to another firm that you don't want to work with.

Some venture capitalists and angel investors may want to be more involved in the workings of your game than a bank would. That means that when you enter into an equity financing agreement, you need to make sure that the investor has a similar vision of your company's future.

Revenue-based financing vs a publishing deal

Securing a publishing deal with revenue sharing is in some ways similar to equity financing in many ways. You can typically leverage publisher resources, relationships and support with UA, monetization, design, etc. While they typically provide a lot of support, they may take a large slice of the revenue pie and have input into building, managing and then scaling the game.

We’ll cover publishing deals more in depth in later articles.

Why choose revenue-based financing?

Generally, revenue-based financing is considered something of a middle ground between debt and equity financing. It's similar to debt financing in that you pay back a total financing amount you received over time without having to hand over ownership in your company, and it's similar to equity financing in that the investor makes revenue when you make revenue.

Business owners typically choose to pursue revenue-based financing when they want the flexibility of equity financing without having to give up any ownership in their company. Investors that offer revenue-based financing also tend to be more hands-off than venture capitalists but more involved than banks, offering a happy medium between the two.

Overall, revenue-based funding is particularly popular among SaaS and e-commerce companies because their revenue stream works well for this type of financing. However, it is equally well-suited to all business models with recurring revenue, like some apps and games.

Revenue-based financing example

Now that we've got a better understanding of revenue-based financing, let's revisit the example from earlier with some (slightly) more realistic numbers. We'll imagine that same advance for $100,000 ($120,000 total with fees) that's paid back as 30% of future revenue.

As you can see, the amount paid each month scaled with revenue growth (or contraction), which some businesses may find preferable to having to pay back a flat fee every month.

Overall, it’s a solid alternative to banks that doesn’t force you to give up part of your company.

Choosing the right revenue-based financing firm

If you decide that RBF is the right direction to go in for your game or app financing, then it’s important to work with a company that not only knows financing in and out, but also understands the specific needs of game and app development so the terms and paybacks of the financing is in sync with the monetization mechanics and dynamics of your product.

When you decide to take your app or game company to the next level (no pun intended), it often means that it's time to look into how to finance it. But with so many options to choose from, ranging from traditional business loans to equity financing to publishing and beyond, entering this stage in your business's growth can quickly turn from an exciting milestone to a nerve-wracking decision.

Chances are that when you think "financing," you imagine one of three things: either you trade a stake in your company for an investment (equity financing), get a bank loan (debt financing), or secure a publishing deal that comes with an advance.

But there's another option that you may not have heard of: revenue-based financing. This financing structure allows for greater flexibility and affordability without having to give up any stake in your company or creative ownership of building games and apps.

What is revenue-based financing?

Revenue-based financing (RBF) is a financing structure in which a company agrees to pay a percentage of its monthly revenue to a capital provider in exchange for a financing. Once the company has paid back the full amount, the company has no remaining obligations to the capital provider. However, if they like working with each other, they can continue developing their relationship through further financing agreements for continued scaling.

Let's look at an example with very simple numbers to make this a bit clearer. Let's say you run a gaming company that makes $50,000/month in revenue, and a capital provider offers to give you an advance for $100,000 in capital at a $120,000 total repayment amount in exchange for 30% of your monthly revenue. How would this play out?

In this case, you'd pay the capital provider $15,000 every month (0.30 * $50,000), and it would take you 8 months to pay them back entirely. But once those 8 months are up, your obligations are met, and you retain full control of your company (assuming you haven't made any other arrangements). If your revenues decrease, so does your repayment amount and vice versa.

Revenue-based financing vs debt financing

Based on the above example alone, the differences between revenue-based and debt financing like a traditional term loan may not seem immediately obvious. After all, isn't a bank loan essentially just a fixed-percentage payment made every month until the loan is paid back?

In our oversimplified example, it's true that they're pretty much identical. But in reality, no business makes exactly the same amount of revenue every month. Especially in the early stages of a business, there may be months where revenues are unusually high followed by severe and sudden downturns.

When repaying a bank loan, you have to make the same payment every month irrespective of whether your business makes $50,000 or $0 in that period. But with revenue-based funding, your monthly payment amount scales with your revenue, which can help your business stay afloat in turbulent waters.

In other words, when you take out a bank loan, it's possible that your monthly payment could end up being more than your entire revenue for the month. With RBF, that would never happen.

However, keep in mind that when you take out a traditional loan, you typically have a fixed term — i.e., you'll pay $2,000 every month for two years. But with RBF, the monthly payment fluctuations mean that it's difficult to determine when the loan amount will be paid back in full (some investors will set predetermined termination dates instead of predetermined amounts, but this is less common). Theoretically, if your revenue were high enough, you could pay back the whole thing in one month, but if business became very slow, you could end up paying back the loan in small increments over a long time period until business picks back up. In the extreme case of a month when you don’t generate any revenue, there is no repayment to the RFB partner.

This uncertainty is why it’s important to work with an RBF partner that has specific game industry experience. They’ll be able to more accurately predict how long it will take you to pay back your financing amount, which will help protect you against biting off more than you can chew.

Revenue-based financing vs equity financing

So, traditional debt financing like a term loan usually means fixed payments over a fixed timeframe while revenue-based financing means paying a fixed percentage of future revenue over an indeterminate time frame.

But what about equity financing? Equity financing solves some of the issues with debt financing, but it brings problems of its own: you're giving away a part of your company.

When you choose to go with equity financing, an investor will give you an initial investment of growth capital for your game or app. You don't have to make monthly payments at all, but you have to be prepared to give a person or a company (a venture capital firm or angel investor, for example) a percentage of direct ownership in your company. The investor will then maintain that equity either forever or until they decide to sell it — which at times may end up being to another firm that you don't want to work with.

Some venture capitalists and angel investors may want to be more involved in the workings of your game than a bank would. That means that when you enter into an equity financing agreement, you need to make sure that the investor has a similar vision of your company's future.

Revenue-based financing vs a publishing deal

Securing a publishing deal with revenue sharing is in some ways similar to equity financing in many ways. You can typically leverage publisher resources, relationships and support with UA, monetization, design, etc. While they typically provide a lot of support, they may take a large slice of the revenue pie and have input into building, managing and then scaling the game.

We’ll cover publishing deals more in depth in later articles.

Why choose revenue-based financing?

Generally, revenue-based financing is considered something of a middle ground between debt and equity financing. It's similar to debt financing in that you pay back a total financing amount you received over time without having to hand over ownership in your company, and it's similar to equity financing in that the investor makes revenue when you make revenue.

Business owners typically choose to pursue revenue-based financing when they want the flexibility of equity financing without having to give up any ownership in their company. Investors that offer revenue-based financing also tend to be more hands-off than venture capitalists but more involved than banks, offering a happy medium between the two.

Overall, revenue-based funding is particularly popular among SaaS and e-commerce companies because their revenue stream works well for this type of financing. However, it is equally well-suited to all business models with recurring revenue, like some apps and games.

Revenue-based financing example

Now that we've got a better understanding of revenue-based financing, let's revisit the example from earlier with some (slightly) more realistic numbers. We'll imagine that same advance for $100,000 ($120,000 total with fees) that's paid back as 30% of future revenue.

As you can see, the amount paid each month scaled with revenue growth (or contraction), which some businesses may find preferable to having to pay back a flat fee every month.

Overall, it’s a solid alternative to banks that doesn’t force you to give up part of your company.

Choosing the right revenue-based financing firm

If you decide that RBF is the right direction to go in for your game or app financing, then it’s important to work with a company that not only knows financing in and out, but also understands the specific needs of game and app development so the terms and paybacks of the financing is in sync with the monetization mechanics and dynamics of your product.

Get a demo

Get a tour of the Sanlo platform!

Get a demo

Get a tour of the Sanlo platform!

Get a demo

Get a tour of the Sanlo platform!

Expert resources that you don't want to miss

Featured

© Sanlo Technologies Inc. 2025.

For game developers, by game developers.

© Sanlo Technologies Inc. 2025.

For game developers, by game developers.

© Sanlo, Inc. 2025. For game developers, by game developers.