How Automation Can Streamline and Reduce Bias in the Funding Process | Sanlo

How Automation Can Streamline and Reduce Bias in the Funding Process | Sanlo

Best Practices

Dec 12, 2022

Dec 12, 2022

Dec 12, 2022

4 mins read

4 mins read

4 mins read

Over time, the route to external financing has become a standardized, inefficient process. Founders will go to venture capitalists or wealthy ‘angels’, map out their vision, and ask for funding in return for a stake in the business. Investors will do their own research and deals will always hinge on subjectivity. Entrepreneurs must persuade investors that their company mission warrants backing, and that they as individuals are capable of making it a reality. Despite the advanced technologies and sectors that investors bankroll, these existing methods are outdated and not fit for purpose. The resolution is to deploy automated AI.

The case for automation in funding processes

In all other areas of finance, there have been huge leaps in data usage over the last decade, from investment platforms to insurance. Now these financial tools are modernizing the startup funding process, automating typically drawn-out processes like calculations of monetary provisions or the exact valuation of a company. This saves investors and businesses valuable hours and resources with capital providers making more objective decisions grounded in metrics and benchmarks instead of solely subjective opinion. Data more accurately informs revenue and industry growth projections and risk profiles, allowing financiers to harness valuable insights into the past, current and future lucrativeness of products and potential investments.

In sectors like SaaS and e-commerce, in which new businesses can quickly attain revenue, success metrics can now be calculated instantaneously. In these verticals, data-driven financing has already become mainstream, whereas sectors with delayed profitability, like gaming, traditionally lag behind. Despite the abundance of data available, it’s often hard to gauge how successful a creative or consumer tech business will be when they start out. As more data and industry figures emerge, investors are better placed to forecast future returns.

How AI and automation work in funding processes

The increasing use of digital tools and a data-driven approach in company financing is more objective, making returns more reliable. Deciding a company’s market valuation, for example, has become a wearisome tug-of-war where investors and founders battle to get the terms most suited to them, eventually meeting somewhere in the middle. An automated, fair judgement expedites this process and gives both parties an agreeable outcome.

There are upsides for investors as well. Using data that generates more accurate projections in funding will give capital providers greater confidence in their choices. Data serves to benchmark what already exists, painting a quantifiable picture. The biases that are ingrained into ‘instinct’ and ‘intuition’ skew judgements and can spawn unwise investments. Data provides precious insights into the previous and future product success, which is especially pivotal to the tech sectors where monetization takes time.

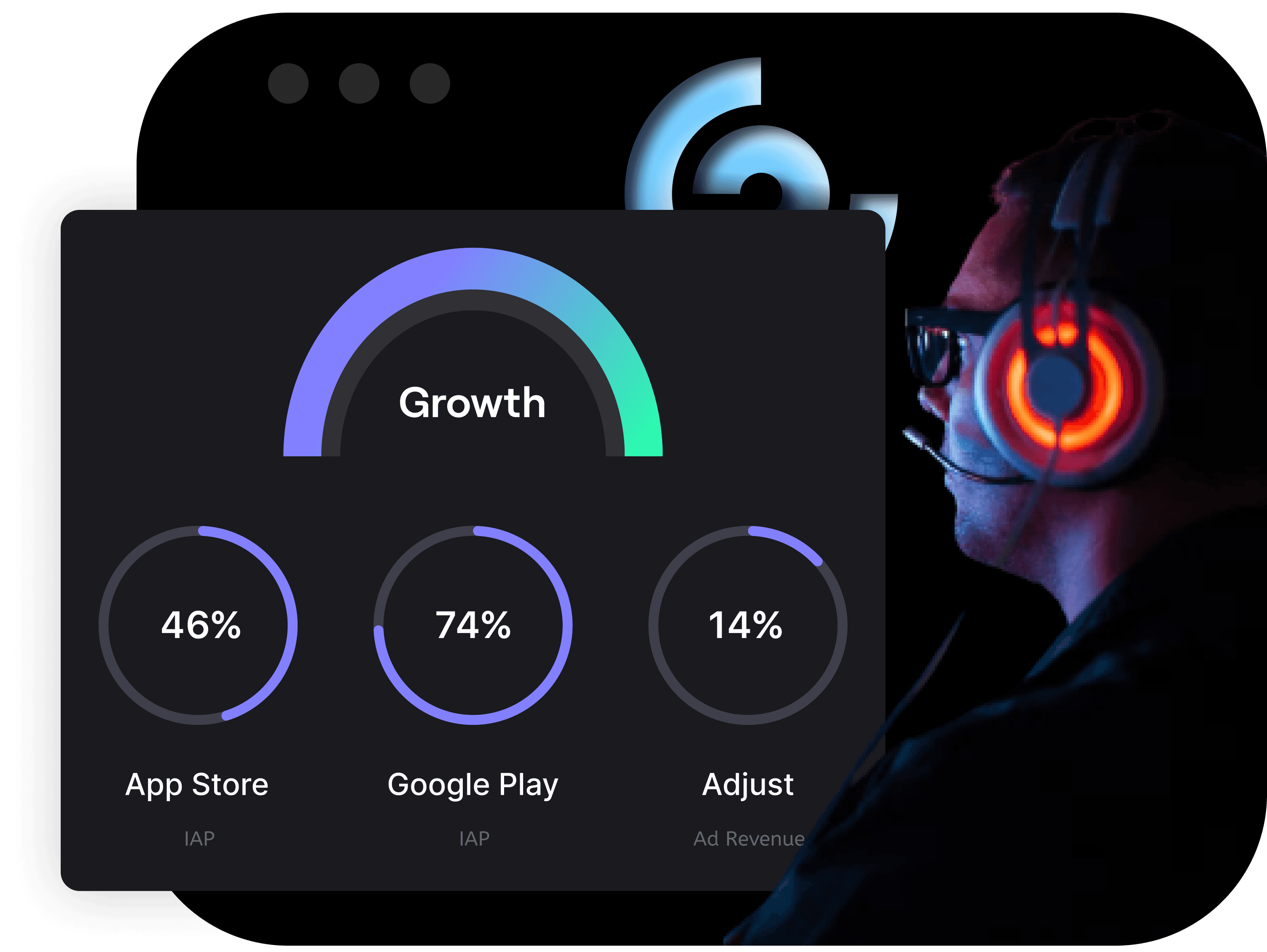

AI and machine learning (ML) is also increasingly deployed in credit and risk functions within financial institutions to help determine credit worthiness of borrowers. With more data becoming readily available on the Internet through APIs, new opportunities are discoverable for AI-driven financial institutions to draw deeper insights into credit applications. For example, in the app economy the credit worthiness (and revenue) of a developer can be predicted using AI, by consuming the app’s product data regarding acquisition, retention and monetization metrics. This cause-and-effect relationship in data is common in predictive analytics.

One can combine this new dimension of financial data, app developers’ individual product performance, with the financial data obtained from the developer’s company’s financial transactions to improve the overall credit worthiness accuracy. Therefore, financial institutions can facilitate financing with higher objectivity and precision.

The drawbacks of bias in existing funding processes

Most budding tech startups initially focus on creating world-class products rather than building out business infrastructure. Founders are often experts in their fields and sometimes recruit like-minded team members with their product in mind so that when the time comes to raise funding and scale, they are left ill-equipped to navigate complex financing processes. There are, however, obvious exceptions to the rule, such as in fintech, where proposed products and financial know-how go hand-in-hand.

Yet many founders lack the financial toolkits that could enable swifter and fairer outcomes. The existing VC system is sluggish and too often reliant on guesswork, blind faith and gut instinct. This can ultimately result in companies with a clear product market fit and a route to growth not receiving the financing that they both need and are worthy of, with primary obstacles centering on access to financing.

Networks become pivotal to entrepreneurs, and newer, ‘green’ founders can be left out of the room. Larger companies or well-known entrepreneurs will always be better placed to obtain financing because of their existing track record, coming at the expense of companies with the right product and target market that lose out because their founders are ‘unknown quantities’. Thus, accessible AI-driven digital tools can give those without the connections opportunities to be judged on their company, not their personality, and perhaps dispel some ‘boys clubs’ stereotypes about the investment community along the way.

Getting in front of investors is difficult enough for entrepreneurs, but the whole financing process is arduous and eats into time they do not have. Pitching, negotiating and finalizing can take months, with the terms unclear to business owners, sometimes taking creative and directional control away. Nobody starts a company to be diluted or in debt, nor to spend months debating every last cent. Data becoming integral to financing will give startups more frictionless access to cash so they can spend their time doing what they originally started their company to do.

Although funding has become a standardized process, it’s important to remember that the tech sector encompasses myriad verticals, and data shouldn’t entirely replace current procedures. Lessening reliances on subjective opinion concerning company missions or founding members and primarily relying on data for investment means that the quality of data is imperative. If the collection process or interpretation is flawed, then any subsequent outcome could be skewed. Data should work to make the funding process swift, objective and painless, but not overthrow it entirely.

Given its upside, many might question why all companies and investors aren’t using data in the funding process. The tools exist, but business owners are often unaware of options available to them, particularly when their company is in its infancy. To improve uptake, we need an educational uplift that empowers budding businesses to make smarter financing decisions.

Analytics are transforming financial decisions at all business stages, and data is helping leaders identify how to maximize their funding to give their businesses the best chances for profitability. Through software development kits, these financial toolkits can now be embedded into easy-to-use platforms. With this data at their fingertips, entrepreneurs have the best chance of success they’ve ever had.

Over time, the route to external financing has become a standardized, inefficient process. Founders will go to venture capitalists or wealthy ‘angels’, map out their vision, and ask for funding in return for a stake in the business. Investors will do their own research and deals will always hinge on subjectivity. Entrepreneurs must persuade investors that their company mission warrants backing, and that they as individuals are capable of making it a reality. Despite the advanced technologies and sectors that investors bankroll, these existing methods are outdated and not fit for purpose. The resolution is to deploy automated AI.

The case for automation in funding processes

In all other areas of finance, there have been huge leaps in data usage over the last decade, from investment platforms to insurance. Now these financial tools are modernizing the startup funding process, automating typically drawn-out processes like calculations of monetary provisions or the exact valuation of a company. This saves investors and businesses valuable hours and resources with capital providers making more objective decisions grounded in metrics and benchmarks instead of solely subjective opinion. Data more accurately informs revenue and industry growth projections and risk profiles, allowing financiers to harness valuable insights into the past, current and future lucrativeness of products and potential investments.

In sectors like SaaS and e-commerce, in which new businesses can quickly attain revenue, success metrics can now be calculated instantaneously. In these verticals, data-driven financing has already become mainstream, whereas sectors with delayed profitability, like gaming, traditionally lag behind. Despite the abundance of data available, it’s often hard to gauge how successful a creative or consumer tech business will be when they start out. As more data and industry figures emerge, investors are better placed to forecast future returns.

How AI and automation work in funding processes

The increasing use of digital tools and a data-driven approach in company financing is more objective, making returns more reliable. Deciding a company’s market valuation, for example, has become a wearisome tug-of-war where investors and founders battle to get the terms most suited to them, eventually meeting somewhere in the middle. An automated, fair judgement expedites this process and gives both parties an agreeable outcome.

There are upsides for investors as well. Using data that generates more accurate projections in funding will give capital providers greater confidence in their choices. Data serves to benchmark what already exists, painting a quantifiable picture. The biases that are ingrained into ‘instinct’ and ‘intuition’ skew judgements and can spawn unwise investments. Data provides precious insights into the previous and future product success, which is especially pivotal to the tech sectors where monetization takes time.

AI and machine learning (ML) is also increasingly deployed in credit and risk functions within financial institutions to help determine credit worthiness of borrowers. With more data becoming readily available on the Internet through APIs, new opportunities are discoverable for AI-driven financial institutions to draw deeper insights into credit applications. For example, in the app economy the credit worthiness (and revenue) of a developer can be predicted using AI, by consuming the app’s product data regarding acquisition, retention and monetization metrics. This cause-and-effect relationship in data is common in predictive analytics.

One can combine this new dimension of financial data, app developers’ individual product performance, with the financial data obtained from the developer’s company’s financial transactions to improve the overall credit worthiness accuracy. Therefore, financial institutions can facilitate financing with higher objectivity and precision.

The drawbacks of bias in existing funding processes

Most budding tech startups initially focus on creating world-class products rather than building out business infrastructure. Founders are often experts in their fields and sometimes recruit like-minded team members with their product in mind so that when the time comes to raise funding and scale, they are left ill-equipped to navigate complex financing processes. There are, however, obvious exceptions to the rule, such as in fintech, where proposed products and financial know-how go hand-in-hand.

Yet many founders lack the financial toolkits that could enable swifter and fairer outcomes. The existing VC system is sluggish and too often reliant on guesswork, blind faith and gut instinct. This can ultimately result in companies with a clear product market fit and a route to growth not receiving the financing that they both need and are worthy of, with primary obstacles centering on access to financing.

Networks become pivotal to entrepreneurs, and newer, ‘green’ founders can be left out of the room. Larger companies or well-known entrepreneurs will always be better placed to obtain financing because of their existing track record, coming at the expense of companies with the right product and target market that lose out because their founders are ‘unknown quantities’. Thus, accessible AI-driven digital tools can give those without the connections opportunities to be judged on their company, not their personality, and perhaps dispel some ‘boys clubs’ stereotypes about the investment community along the way.

Getting in front of investors is difficult enough for entrepreneurs, but the whole financing process is arduous and eats into time they do not have. Pitching, negotiating and finalizing can take months, with the terms unclear to business owners, sometimes taking creative and directional control away. Nobody starts a company to be diluted or in debt, nor to spend months debating every last cent. Data becoming integral to financing will give startups more frictionless access to cash so they can spend their time doing what they originally started their company to do.

Although funding has become a standardized process, it’s important to remember that the tech sector encompasses myriad verticals, and data shouldn’t entirely replace current procedures. Lessening reliances on subjective opinion concerning company missions or founding members and primarily relying on data for investment means that the quality of data is imperative. If the collection process or interpretation is flawed, then any subsequent outcome could be skewed. Data should work to make the funding process swift, objective and painless, but not overthrow it entirely.

Given its upside, many might question why all companies and investors aren’t using data in the funding process. The tools exist, but business owners are often unaware of options available to them, particularly when their company is in its infancy. To improve uptake, we need an educational uplift that empowers budding businesses to make smarter financing decisions.

Analytics are transforming financial decisions at all business stages, and data is helping leaders identify how to maximize their funding to give their businesses the best chances for profitability. Through software development kits, these financial toolkits can now be embedded into easy-to-use platforms. With this data at their fingertips, entrepreneurs have the best chance of success they’ve ever had.

Over time, the route to external financing has become a standardized, inefficient process. Founders will go to venture capitalists or wealthy ‘angels’, map out their vision, and ask for funding in return for a stake in the business. Investors will do their own research and deals will always hinge on subjectivity. Entrepreneurs must persuade investors that their company mission warrants backing, and that they as individuals are capable of making it a reality. Despite the advanced technologies and sectors that investors bankroll, these existing methods are outdated and not fit for purpose. The resolution is to deploy automated AI.

The case for automation in funding processes

In all other areas of finance, there have been huge leaps in data usage over the last decade, from investment platforms to insurance. Now these financial tools are modernizing the startup funding process, automating typically drawn-out processes like calculations of monetary provisions or the exact valuation of a company. This saves investors and businesses valuable hours and resources with capital providers making more objective decisions grounded in metrics and benchmarks instead of solely subjective opinion. Data more accurately informs revenue and industry growth projections and risk profiles, allowing financiers to harness valuable insights into the past, current and future lucrativeness of products and potential investments.

In sectors like SaaS and e-commerce, in which new businesses can quickly attain revenue, success metrics can now be calculated instantaneously. In these verticals, data-driven financing has already become mainstream, whereas sectors with delayed profitability, like gaming, traditionally lag behind. Despite the abundance of data available, it’s often hard to gauge how successful a creative or consumer tech business will be when they start out. As more data and industry figures emerge, investors are better placed to forecast future returns.

How AI and automation work in funding processes

The increasing use of digital tools and a data-driven approach in company financing is more objective, making returns more reliable. Deciding a company’s market valuation, for example, has become a wearisome tug-of-war where investors and founders battle to get the terms most suited to them, eventually meeting somewhere in the middle. An automated, fair judgement expedites this process and gives both parties an agreeable outcome.

There are upsides for investors as well. Using data that generates more accurate projections in funding will give capital providers greater confidence in their choices. Data serves to benchmark what already exists, painting a quantifiable picture. The biases that are ingrained into ‘instinct’ and ‘intuition’ skew judgements and can spawn unwise investments. Data provides precious insights into the previous and future product success, which is especially pivotal to the tech sectors where monetization takes time.

AI and machine learning (ML) is also increasingly deployed in credit and risk functions within financial institutions to help determine credit worthiness of borrowers. With more data becoming readily available on the Internet through APIs, new opportunities are discoverable for AI-driven financial institutions to draw deeper insights into credit applications. For example, in the app economy the credit worthiness (and revenue) of a developer can be predicted using AI, by consuming the app’s product data regarding acquisition, retention and monetization metrics. This cause-and-effect relationship in data is common in predictive analytics.

One can combine this new dimension of financial data, app developers’ individual product performance, with the financial data obtained from the developer’s company’s financial transactions to improve the overall credit worthiness accuracy. Therefore, financial institutions can facilitate financing with higher objectivity and precision.

The drawbacks of bias in existing funding processes

Most budding tech startups initially focus on creating world-class products rather than building out business infrastructure. Founders are often experts in their fields and sometimes recruit like-minded team members with their product in mind so that when the time comes to raise funding and scale, they are left ill-equipped to navigate complex financing processes. There are, however, obvious exceptions to the rule, such as in fintech, where proposed products and financial know-how go hand-in-hand.

Yet many founders lack the financial toolkits that could enable swifter and fairer outcomes. The existing VC system is sluggish and too often reliant on guesswork, blind faith and gut instinct. This can ultimately result in companies with a clear product market fit and a route to growth not receiving the financing that they both need and are worthy of, with primary obstacles centering on access to financing.

Networks become pivotal to entrepreneurs, and newer, ‘green’ founders can be left out of the room. Larger companies or well-known entrepreneurs will always be better placed to obtain financing because of their existing track record, coming at the expense of companies with the right product and target market that lose out because their founders are ‘unknown quantities’. Thus, accessible AI-driven digital tools can give those without the connections opportunities to be judged on their company, not their personality, and perhaps dispel some ‘boys clubs’ stereotypes about the investment community along the way.

Getting in front of investors is difficult enough for entrepreneurs, but the whole financing process is arduous and eats into time they do not have. Pitching, negotiating and finalizing can take months, with the terms unclear to business owners, sometimes taking creative and directional control away. Nobody starts a company to be diluted or in debt, nor to spend months debating every last cent. Data becoming integral to financing will give startups more frictionless access to cash so they can spend their time doing what they originally started their company to do.

Although funding has become a standardized process, it’s important to remember that the tech sector encompasses myriad verticals, and data shouldn’t entirely replace current procedures. Lessening reliances on subjective opinion concerning company missions or founding members and primarily relying on data for investment means that the quality of data is imperative. If the collection process or interpretation is flawed, then any subsequent outcome could be skewed. Data should work to make the funding process swift, objective and painless, but not overthrow it entirely.

Given its upside, many might question why all companies and investors aren’t using data in the funding process. The tools exist, but business owners are often unaware of options available to them, particularly when their company is in its infancy. To improve uptake, we need an educational uplift that empowers budding businesses to make smarter financing decisions.

Analytics are transforming financial decisions at all business stages, and data is helping leaders identify how to maximize their funding to give their businesses the best chances for profitability. Through software development kits, these financial toolkits can now be embedded into easy-to-use platforms. With this data at their fingertips, entrepreneurs have the best chance of success they’ve ever had.

Get a demo

Get a tour of the Sanlo platform!

Get a demo

Get a tour of the Sanlo platform!

Get a demo

Get a tour of the Sanlo platform!

Expert resources that you don't want to miss

Featured

Automation in Funding: Streamlining and Reducing Bias

Streamline and Reduce Bias in the Funding Process with Automation

© Sanlo Technologies Inc. 2025.

For game developers, by game developers.

Automation in Funding: Streamlining and Reducing Bias

Streamline and Reduce Bias in the Funding Process with Automation

© Sanlo, Inc. 2025. For game developers, by game developers.